Matbiips example: Stochastic volatility

In this example, we consider the stochastic volatility model SV0 for application e.g. in finance.

Reference: S. Chib, F. Nardari, N. Shepard. Markov chain Monte Carlo methods for stochastic volatility models. Journal of econometrics, vol. 108, pp. 281-316, 2002.

Contents

Statistical model

The stochastic volatility model is defined as follows

and for

where  is the response variable and

is the response variable and  is the unobserved log-volatility of .

is the unobserved log-volatility of .  denotes the normal distribution of mean

denotes the normal distribution of mean  and variance

and variance  .

.

,

,  and

and  are unknown parameters that need to be estimated.

are unknown parameters that need to be estimated.

Statistical model in BUGS language

Content of the file 'stoch_volatility.bug':

model_file = 'stoch_volatility.bug'; % BUGS model filename type(model_file);

# Stochastic volatility model SV_0

# Reference: S. Chib, F. Nardari, N. Shepard. Markov chain Monte Carlo methods

# for stochastic volatility models. Journal of econometrics, vol. 108, pp. 281-316, 2002.

var y[t_max], x[t_max], prec_y[t_max]

data

{

x_true[1] ~ dnorm(0, 1/sigma_true^2)

prec_y_true[1] <- exp(-x_true[1])

y[1] ~ dnorm(0, prec_y_true[1])

for (t in 2:t_max)

{

x_true[t] ~ dnorm(alpha_true + beta_true*(x_true[t-1]-alpha_true), 1/sigma_true^2)

prec_y_true[t] <- exp(-x_true[t])

y[t] ~ dnorm(0, prec_y_true[t])

}

}

model

{

alpha ~ dnorm(0,10000)

logit_beta ~ dnorm(0,.1)

beta <- ilogit(logit_beta)

log_sigma ~ dnorm(0, 1)

sigma <- exp(log_sigma)

x[1] ~ dnorm(0, 1/sigma^2)

prec_y[1] <- exp(-x[1])

y[1] ~ dnorm(0, prec_y[1])

for (t in 2:t_max)

{

x[t] ~ dnorm(alpha + beta*(x[t-1]-alpha), 1/sigma^2)

prec_y[t] <- exp(-x[t])

y[t] ~ dnorm(0, prec_y[t])

}

}

Installation of Matbiips

- Download the latest version of Matbiips

- Unzip the archive in some folder

- Add the Matbiips folder to the Matlab search path

matbiips_path = '../../matbiips';

addpath(matbiips_path)

General settings

set(0, 'DefaultAxesFontsize', 14); set(0, 'Defaultlinelinewidth', 2); light_blue = [.7, .7, 1]; % Set the random numbers generator seed for reproducibility if isoctave() || verLessThan('matlab', '7.12') rand('state', 0) else rng('default') end

Load model and load or simulate data

sample_data = true; % Simulated data or SP500 data t_max = 100; if ~sample_data % Load the data T = readtable('SP500.csv', 'delimiter', ';'); y = diff(log(T.Close(end:-1:1))); SP500_date_str = T.Date(end:-1:2); ind = 1:t_max; y = y(ind); SP500_date_str = SP500_date_str(ind); SP500_date_num = datenum(SP500_date_str); end

Model parameters

if ~sample_data data = struct('t_max', t_max, 'y', y); else sigma_true = .4; alpha_true = 0; beta_true = .99; data = struct('t_max', t_max, 'sigma_true', sigma_true,... 'alpha_true', alpha_true, 'beta_true', beta_true); end

Compile BUGS model and sample data if simulated data

model = biips_model(model_file, data, 'sample_data', sample_data);

data = model.data;

* Parsing model in: stoch_volatility.bug * Compiling data graph Declaring variables Resolving undeclared variables Allocating nodes Graph size: 706 Sampling data Reading data back into data table * Compiling model graph Declaring variables Resolving undeclared variables Allocating nodes Graph size: 715

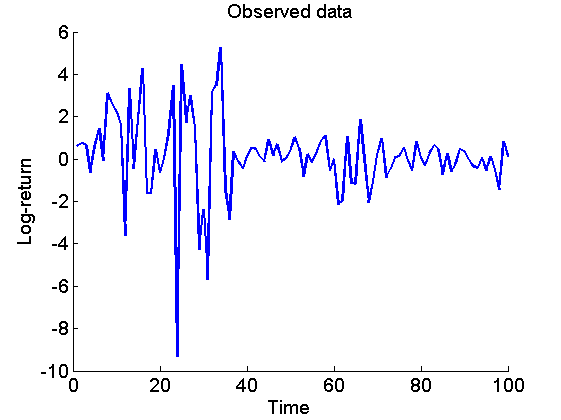

Plot the data

figure('name', 'Log-returns') if sample_data plot(1:t_max, data.y) title('Observed data') xlabel('Time') else plot(SP500_date_num, data.y) title('Observed data: S&P 500') datetick('x', 'mmmyyyy', 'keepticks') xlabel('Date') end ylabel('Log-return') box off

Biips Particle Marginal Metropolis-Hastings

We now use Biips to run a Particle Marginal Metropolis-Hastings in order to obtain posterior MCMC samples of the parameters , and , and of the variables  .

.

Parameters of the PMMH

n_burn = 5000; % nb of burn-in/adaptation iterations n_iter = 10000; % nb of iterations after burn-in thin = 5; % thinning of MCMC outputs n_part = 50; % nb of particles for the SMC param_names = {'alpha', 'logit_beta', 'log_sigma'}; % names of the variables updated with MCMC (others are updated with SMC) latent_names = {'x'}; % names of the variables updated with SMC and that need to be monitored

Init PMMH

inits = {0, 5, -2};

obj_pmmh = biips_pmmh_init(model, param_names, 'inits', inits,...

'latent_names', latent_names);

* Initializing PMMH

Run PMMH

obj_pmmh = biips_pmmh_update(obj_pmmh, n_burn, n_part); % adaptation and burn-in iterations [obj_pmmh, out_pmmh, log_marg_like_pen, log_marg_like] = biips_pmmh_samples(obj_pmmh, n_iter, n_part,... 'thin', thin); % Samples

* Adapting PMMH with 50 particles |--------------------------------------------------| 100% |++++++++++++++++++++++++++++++++++++++++++++++++++| 5000 iterations in 203.25 s * Generating 2000 PMMH samples with 50 particles |--------------------------------------------------| 100% |**************************************************| 10000 iterations in 381.09 s

Some summary statistics

summ_pmmh = biips_summary(out_pmmh, 'probs', [.025, .975]);

Compute kernel density estimates

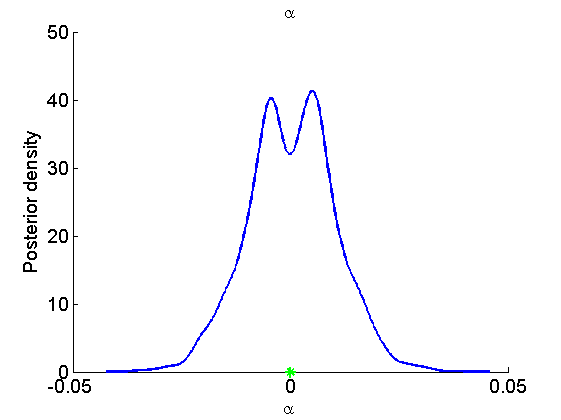

kde_pmmh = biips_density(out_pmmh);

Posterior mean and credible interval of the parameters

for i=1:numel(param_names) summ_param = getfield(summ_pmmh, param_names{i}); fprintf('Posterior mean of %s: %.3f\n', param_names{i}, summ_param.mean); fprintf('95%% credible interval of %s: [%.3f, %.3f]\n',... param_names{i}, summ_param.quant{1}, summ_param.quant{2}); end

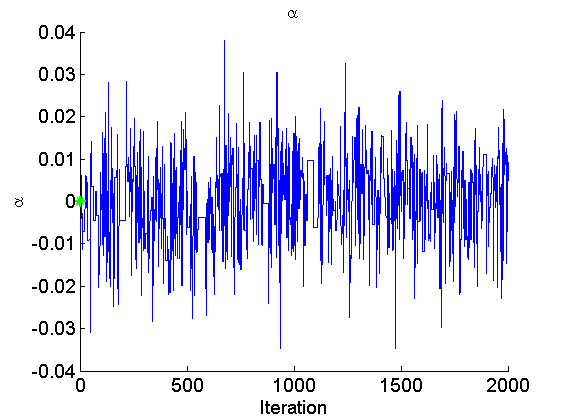

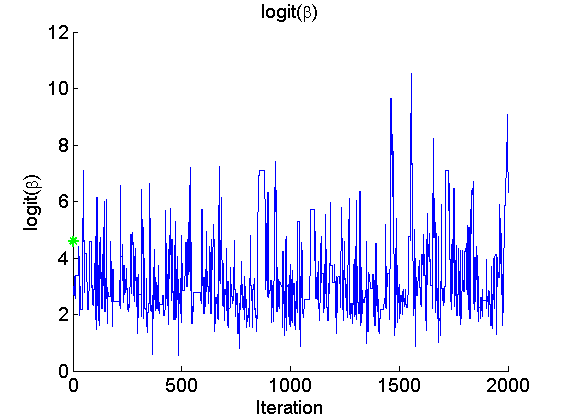

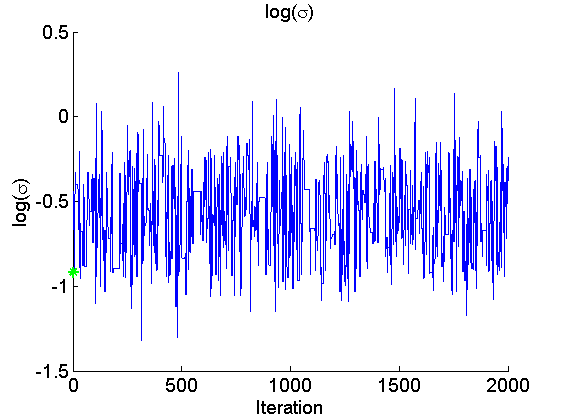

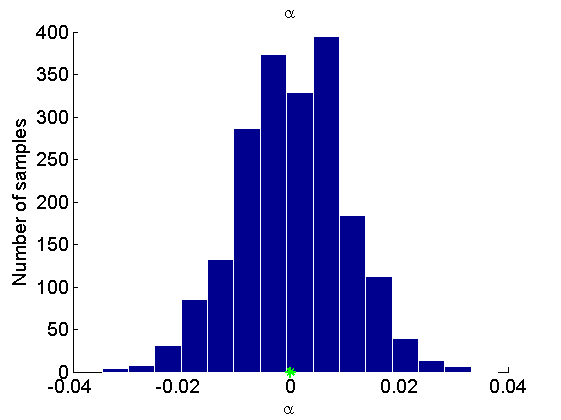

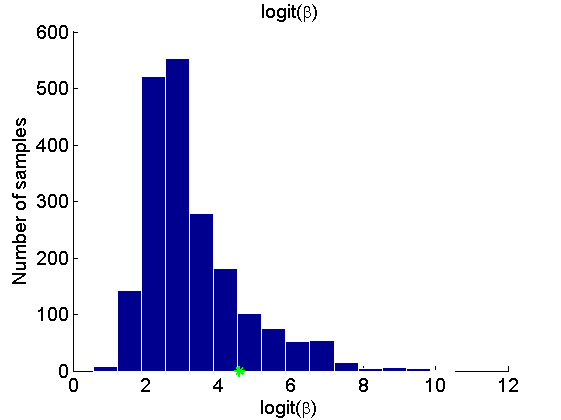

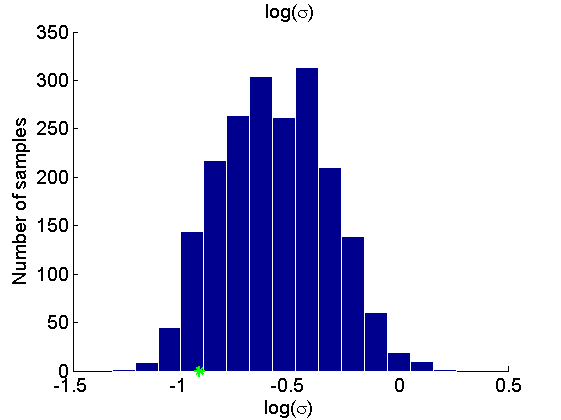

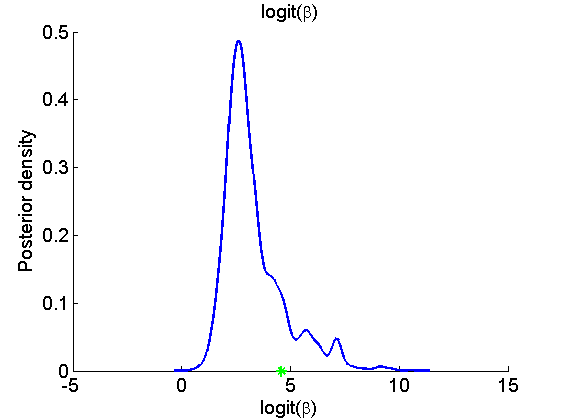

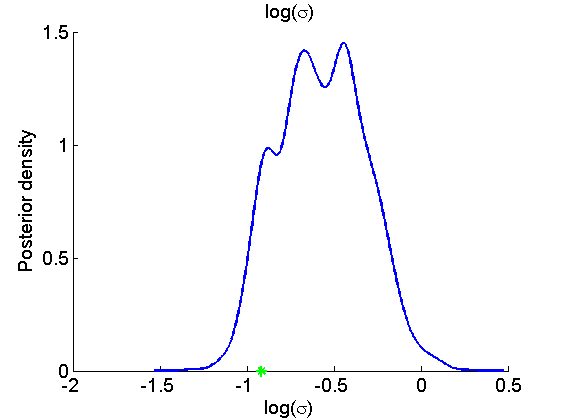

Posterior mean of alpha: 0.000 95% credible interval of alpha: [-0.020, 0.020] Posterior mean of logit_beta: 3.309 95% credible interval of logit_beta: [1.521, 7.178] Posterior mean of log_sigma: -0.571 95% credible interval of log_sigma: [-1.009, -0.110]

Trace of MCMC samples for the parameters

if sample_data param_true = [alpha_true, log(data.beta_true/(1-data.beta_true)), log(sigma_true)]; end param_lab = {'\alpha', 'logit(\beta)', 'log(\sigma)'}; for k=1:numel(param_names) figure('name', 'PMMH: Trace samples parameter') samples_param = getfield(out_pmmh, param_names{k}); plot(samples_param, 'linewidth', 1) if sample_data hold on plot(0, param_true(k), '*g'); end xlabel('Iteration') ylabel(param_lab{k}) title(param_lab{k}) box off legend boxoff end

Histogram and KDE estimate of the posterior for the parameters

for k=1:numel(param_names) figure('name', 'PMMH: Histogram posterior parameter') samples_param = getfield(out_pmmh, param_names{k}); hist(samples_param, 15) h = findobj(gca, 'Type', 'patch'); set(h, 'EdgeColor', 'w') if sample_data hold on plot(param_true(k), 0, '*g'); end xlabel(param_lab{k}) ylabel('Number of samples') title(param_lab{k}) box off legend boxoff end for k=1:numel(param_names) figure('name', 'PMMH: KDE estimate posterior parameter') kde_param = getfield(kde_pmmh, param_names{k}); plot(kde_param.x, kde_param.f) if sample_data hold on plot(param_true(k), 0, '*g'); end xlabel(param_lab{k}) ylabel('Posterior density') title(param_lab{k}) box off legend boxoff end

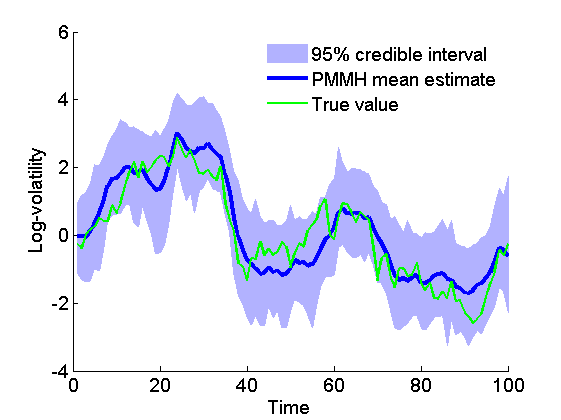

Posterior mean and quantiles for x

figure('name', 'PMMH: Posterior mean and quantiles') x_pmmh_mean = summ_pmmh.x.mean; x_pmmh_quant = summ_pmmh.x.quant; h = fill([1:t_max, t_max:-1:1], [x_pmmh_quant{1}; flipud(x_pmmh_quant{2})], 0); set(h, 'edgecolor', 'none', 'facecolor', light_blue) hold on plot(1:t_max, x_pmmh_mean, 'linewidth', 3) if sample_data plot(1:t_max, data.x_true, 'g') legend({'95% credible interval', 'PMMH mean estimate', 'True value'}) else legend({'95% credible interval', 'PMMH mean estimate'}) end xlabel('Time') ylabel('Log-volatility') box off legend boxoff

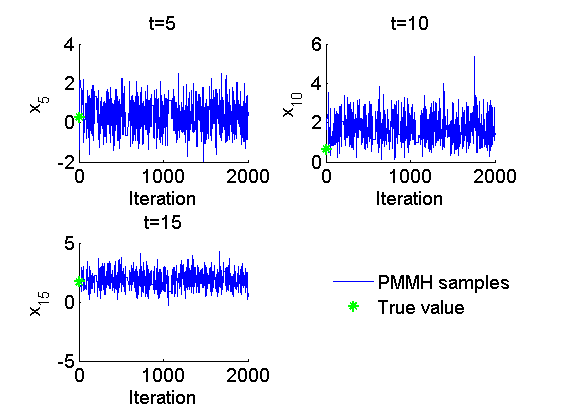

Trace of MCMC samples for x

figure('name', 'PMMH: Trace samples x') time_index = [5, 10, 15]; for k=1:numel(time_index) tk = time_index(k); subplot(2, 2, k) plot(out_pmmh.x(tk, :), 'linewidth', 1) if sample_data hold on plot(0, data.x_true(tk), '*g'); end xlabel('Iteration') ylabel(['x_{', num2str(tk), '}']) title(['t=', num2str(tk)]); box off end if sample_data h = legend({'PMMH samples', 'True value'}); set(h, 'position', [0.7, 0.25, .1, .1]) legend boxoff end

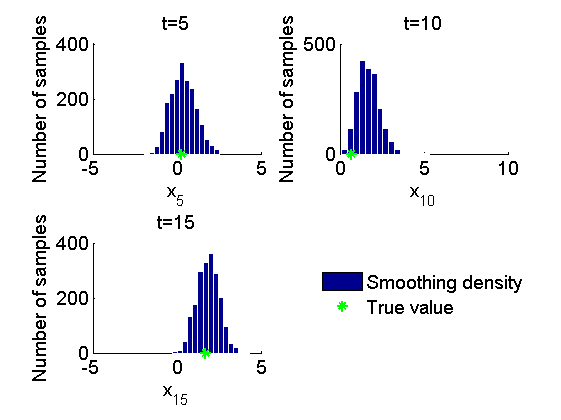

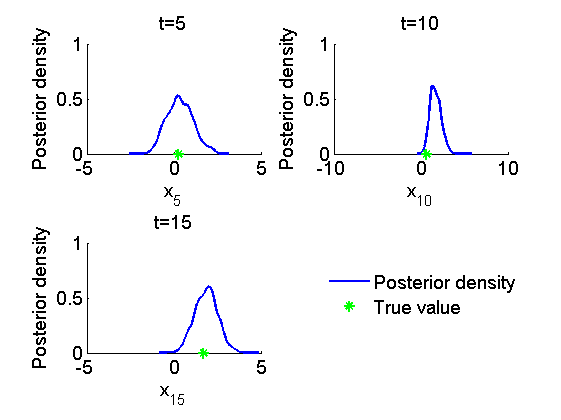

Histogram and kernel density estimate of posteriors of x

figure('name', 'PMMH: Histograms marginal posteriors') for k=1:numel(time_index) tk = time_index(k); subplot(2, 2, k) hist(out_pmmh.x(tk, :), 15); h = findobj(gca, 'Type', 'patch'); set(h, 'EdgeColor', 'w') if sample_data hold on plot(data.x_true(tk), 0, '*g'); end xlabel(['x_{', num2str(tk), '}']); ylabel('Number of samples'); title(['t=', num2str(tk)]); box off end if sample_data h = legend({'Smoothing density', 'True value'}); set(h, 'position', [0.7, 0.25, .1, .1]) legend boxoff end figure('name', 'PMMH: KDE estimates marginal posteriors') for k=1:numel(time_index) tk = time_index(k); subplot(2, 2, k) plot(kde_pmmh.x(tk).x, kde_pmmh.x(tk).f); if sample_data hold on plot(data.x_true(tk), 0, '*g'); end xlabel(['x_{', num2str(tk), '}']); ylabel('Posterior density'); title(['t=', num2str(tk)]); box off end if sample_data h = legend({'Posterior density', 'True value'}); set(h, 'position', [0.7, 0.25, .1, .1]) legend boxoff end

Clear model

biips_clear()